In the quest to generate alpha and improve investment returns, more buy-side firms are adopting multi-asset trading. In this blog post, I will discuss the three major global trends that are driving this shift and their impact on requirements for portfolio and risk management, based on findings from a recent Aite Group survey.

1. Global Market Trends

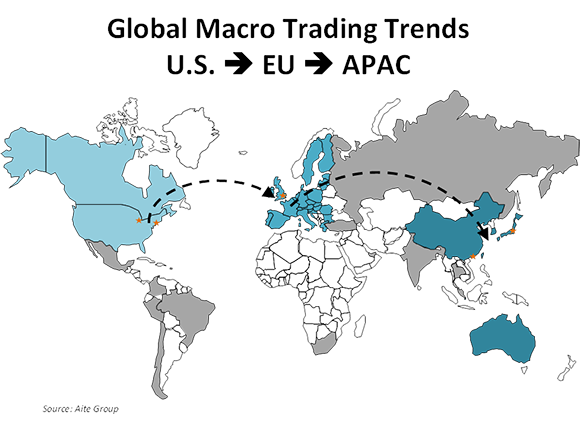

Over the last several decades there has been a consistent evolutionary/migratory pattern of trading structures, technologies, methodologies, market structures, and regulations across regions.

It is common for new trends in trading technology to begin in financial hubs, such as New York or Chicago, where someone pioneers an idea or concept. At some point that concept becomes popular and everyone starts using it throughout North America (NA), therefore commoditizing that idea or concept. Once this happens, typically in three to six years, the concept will jump over to Europe, typically first in London. Then, three to six years after that, it will be picked up in the Asia Pacific (APAC), typically being adopted first in Hong Kong, Singapore, or Tokyo. Ultimately, once a trading concept is commoditized in the U.S., it will take 10 years to propagate to APAC, and from there to the rest of the world.

In 2010, modern multi-asset trading was pioneered in NA. While old-style multi-asset trading involves equities, options, and futures, modern multi-asset trading adds in the use of fixed income, FX, or both. This modern trading style was first adopted by proprietary trading firms and some global macro hedge funds. From that point forward, the new trading style took off globally. In 2015, NA buy-side firms began adopting modern multi-asset trading in earnest, and it soon became commoditized there while the sell-side continued to use old-style multi-asset trading. Around 2013 those same mainly NA firms that pioneered modern multi-asset trading started exploring cross-asset trading, where there are tight correlations across multiple disparate asset classes and products in one’s trades. It’s likely that one to two years from now NA firms using modern multi-asset trading will evolve to cross-asset trading. Inevitably, this shift to cross-asset trading will require more powerful tools for pricing, valuation, and risk.

At the same time this evolution in trading is occurring, markets of all kinds, from OTC platforms to actual listed exchanges, are popping up everywhere in many different asset classes and products. For instance, currently there are more than a dozen swap execution facilities (SEFs), still more new fixed income platforms, many derivatives exchanges, and new cash equities models. Firms want to connect to as many markets as possible in their global search for alpha. As such, firms must consider more than just connectivity. Once they access derivatives and fixed income markets, they also need to aggregate the prices, eventually on a multi-asset basis. This requires heavy-duty technology in many cases.

2. Sell-Side Capital Costs

A second significant global trading trend is the sell-side’s increasing cost of capital, which has risen two to three times since 2008. This has driven much principal trading over to agency trading or brokerage. As a result, much inventory has shifted to the buy-side, and along with it many more responsibilities.

Buy-side firms that once relied on the sell-side for pricing, risk, and valuation now need to do these things themselves. These added responsibilities require technology that buy-sides may not have. Also, while buy-side firms are not necessarily acting as market-makers, they are doing price-making, so they need tools that offer them speedy scenario-based pricing abilities in order to opportunistically make prices and capture promising trading opportunities.

3. Regulation

A third major trend driving firms to multi-asset trading is the impact of regulation. Regulation’s overhead always looms large, but attitudes towards it have recently shifted. While once buy-side firms may have engaged in regulatory arbitrage, today there is a trend toward fuller compliance with regulatory standards in many parts of the world. Instead of firms meeting the lowest regulatory standards in a region, they are reaching for the highest global regulatory bar across regions. For example, if a firm is trading in multiple regions, and it has a stringent best-execution requirement in one region, then it will consider applying that same requirement to all regions in which it trades. For many firms, introducing this consistency is easier than dealing with many different regulations in different regions.

Additionally, regulation is being pushed to a pre-trade basis. This means that buy-side firms need to take on more responsibility in compliance and regulation, which require enhanced price aggregation and corresponding technology updates.

Aite Group’s Shifting Sands Survey

A recent Aite Group study surveyed major Tier-1 and Tier-2 buy- and sell-side firms throughout the world to explore what factors are pushing them in a multi-asset direction. Over half of the respondents averaged more than US$500 billion in trading each year. 43% of those surveyed were buy-side firms, while 57% were sell-sides.

Many buy-side firms surveyed said they engage in a wide range of trading methods. Top among these are electronic, voice, and listed trading. These buy-sides also have a wide range of ways they manage risk, with many doing risk management on a pre-trade basis.

When the buy-side firm respondents were asked whether they had a real-time, pre- and post-trade risk management system in place, half reported they did, while 28% have plans to do so. This trend indicates the majority of firms realize the increased importance of real-time risk management.

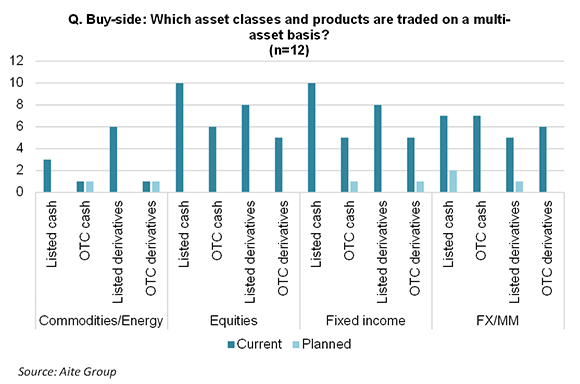

Aite Group’s Shifting Sands survey also found that 76% of buy-side firms are doing multi-asset trading, as indicated in this chart of the diverse asset classes and products traded by these firms on a multi-asset basis.

Additionally, 53% of firms said they have or plan to have shared order books across their trading desks. Of those that do have shared order books, they are often multi-asset in nature. When comparing the two, it becomes clear how the buy-side is leading the sell-side in modern multi-asset trading. Of the firms in the study that reported having shared order books, the buy-sides’ books were more multi-asset, while the sell-sides’ books were more siloed.

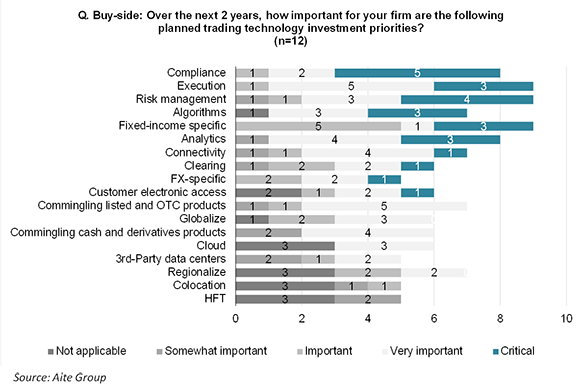

In terms of technology priorities, one might think execution would top the list for buy-side firms. However, the study proved otherwise, as indicated in this chart showing compliance as the top priority, followed by execution and then risk management.

Interestingly, despite the hype around HFT, it fell at the bottom of buy-sides’ priorities.

Furthermore, the buy-sides surveyed reported the top two areas of business growth included expanding into new asset classes and emerging markets. This trend indicates the high priority they place on connecting to as many markets as possible in their global search for alpha.

For more information, watch the on-demand webinar: 5 Top Questions to ask when upgrading your Valuation and Risk System