FINCAD and Tradition recently hosted a joint webinar, SOFR Transition: Current and Future Implications for Derivatives, Loans and Fixed Income. I had the pleasure of co-presenting with Chris McGuigan of Tradition, as we discussed the unfolding events happening now as the US transitions from Libor to SOFR.

The US is currently accelerating its pace to replace the Libor interest rate benchmark. As a result, focus is now turning to SOFR for the future of derivatives, loans, and fixed income securities. It was great having Chris kick off the webinar and update us on the interesting developments on the broker side. I was particularly interested in the recent work Tradition has been doing to bring their clients the SOFR rate sooner than anyone else. Tradition’s new indicative SOFR product is an example of the type of innovation that often takes place when there is such a significant change happening in the market, like what we’re seeing now with Libor.

Later I discussed the Libor fallbacks and how they are both an imminent reality and also something we can test in the markets. SOFR is not without its challenges, as it is a backwards-looking rate (whereas Libor is forward-looking) and there is low derivative availability for hedging, among other challenges. This means things are not quite settled down yet for what will replace Libor in some cases, but using analytics combined with market feeds can give you a clearer picture of what is currently happening in the SOFR transition.

We are now seeing significant moves away from Libor, but for those securities that continue to use Libor until it is no longer published, we can take a closer look at the market-side information. SOFR and Libor are not identical – Libor is a term rate that is fixed in advance, while SOFR is an overnight rate that is averaged in arrears from daily fixings. So, in theory, when Libor is completely discontinued, it could trigger a wide range of alternative rate-based calculations based on SOFR as a replacement, and new challenges await.

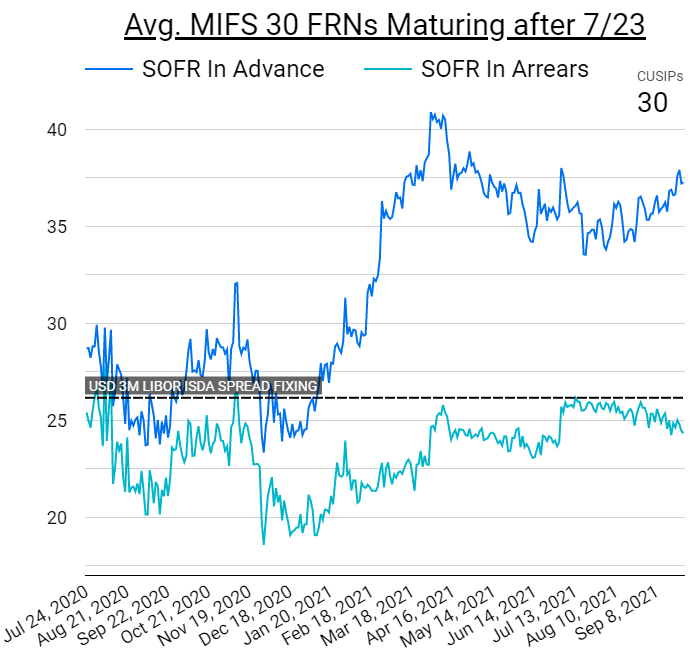

We can learn a lot by looking at how the market is updating its pricing on some of the assets linked to Libor. In the example below, I’ve taken the price of FRNs and used that to calculate the discount margin. This is how I obtained a direct measure of the spread of a FRN to the treasury curve. I’ve calibrated a fallback spread for each bond, every day to bring the price back to par. This is what I call the ‘market-implied fallback spread.’ In the end, I was able to use approximately 30 A+ financial sector FRNs that paid quarterly Libor and that have maturities after the start of July 2023, when the switchover will happen. I calculated the market implied fallback spread every day for every bond for the last couple of years and then averaged all these spreads across all the bonds to arrive at the figure below. For the sake of comparison, I used two different alternative rates, SOFR in-arrears and SOFR in-advance.

These figures and some other interesting results are discussed in the webinar. In short, we are testing the market fallbacks, which can lead to quite a few insights into the current state of the SOFR transition. For example, the underlying forward skew risk and convexity issues with SOFR in-advance I found surprising. And the types of insights discussed in this presentation were built upon high quality market data such as that provided by Tradition. When you combine the tools and expertise of FINCAD Analytics with the latest in market data, you’re afforded many insights, including an inside look at the Libor transition– one that can better enable you to manage risks, match cash flows, find new strategies and move with the liquidity.

Learn More

For additional analysis and discussion on this topic, be sure to check out the full webinar recording here.