It is critical that curves accurately reflect the nature of markets they are intended to describe. If they don’t, you’re probably losing opportunities by lagging the market, trading on bad information, misreporting P&L or misunderstanding risk in your book. Accurate curves can result in competitive advantage. You avoid lag time of assessing multiple dealer quotes, produce independent prices that you can rely on, report the most accurate P&L and get a holistic view of risk across your organization.

One of the first steps to building accurate curves is migrating discounting conventions from LIBOR to OIS.

A New Proxy

In response to the credit crisis, derivative trading has migrated en masse from an over-the-counter to an on-exchange market in an attempt to mitigate counterparty credit exposure.

Prior to 2008, fully collateralized trades were discounted at LIBOR (London Interbank Offered Rate), which was assumed to be an effective proxy of the risk-free rate. But, post-2008, it has been widely recognized that under stressed conditions, LIBOR is not a good proxy. However, relative to LIBOR, OIS (Overnight Index Swap) remained stable during stressed conditions and, consequently, has been adopted as the risk-free rate. Because collateral posted for centrally cleared derivatives accrues interest at the risk-free rate, OIS discounting needs to be considered for these instruments.

However, even for OTC derivatives which are not fully collateralized, OIS discounting is still required for net present value calculations. To account for the fact that these instruments are not risk-free, subsequent valuation adjustments are made for credit, own-credit, and cost of funding, collectively known as the xVAs.

Short End and Long End

For precise OIS curve construction, certain subtleties need to be incorporated to be market-consistent.

One such consideration is that the Federal Open Market Committee meetings do not conveniently align with the maturity dates of standard Overnight Index Swap market data. Since the Federal Reserve controls the policy which defines the Overnight rate, and this rate is effective until the following meeting date, your OIS curve should accurately reflect this reality by shifting vertically up or down on meeting dates, and being flat in between.

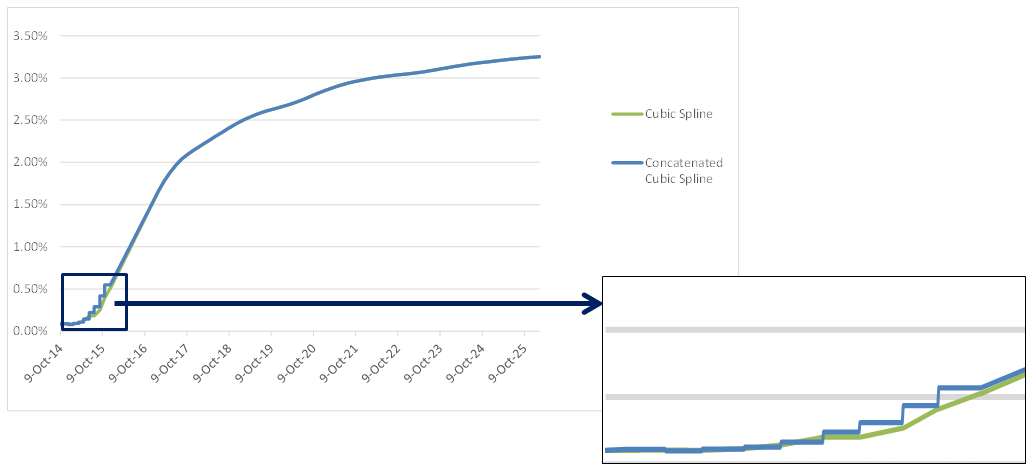

To achieve a flat curve between meeting dates, it’s common to use Log Linear interpolation, as displayed in the short end of the curve in Figure 1.

Flat forward rates are fine between instrument maturities at the short end, but the long end of the curve runs into an additional problem. Because OIS market data becomes sparse - initially 3-month gaps and eventually multi-year gaps - another solution needs to be adopted to maintain accuracy.

To best represent Overnight forward rates at the long end of the curve, you need to introduce a Linear or Smoothing approach. A problem with using multiple interpolation methods for a single curve is that traditional curve building frameworks force users to choose a single method. Without the flexibility to use different interpolation methods for different partitions of the curve, your curve won’t be market-consistent and, subsequently, the accuracy of analytics will suffer. If your analytics are off, you can count on pricing and risk being off as well.

Figure 1 - Log Linear interpolation for curve short end

Stitching the Pieces Together

When calibrating the long end, consistency with the short end must be enforced.

This is done by using the previously calibrated short end of the curve (or curves in the case of a dual calibration) when pricing flows occur in the short tenor. Theoretically speaking, this capability is not too taxing; however, this capability needs to be specifically coded into a curve building framework, unless the framework is already sufficiently flexible and future-proof to all types of calibration.

Figure 1 illustrates this type of concatenation, stitching the short end (boxed) to the long end of the curve.

Dual and Multi Calibration

A capability used often for OIS curve construction is dual (or multi) curve calibration, but this method comes with its own risks. The reason for needing dual calibration is illiquidity. In the U.S., the Overnight Index Swap market becomes less liquid in favor of the LIBOR-Fed Funds basis swap market after about 7 years.

This dual dependence of standard LIBOR swaps and LIBOR-Fed Funds basis swaps on the OIS discount and LIBOR curves creates a curve construction problem which necessitates a multi-curve solver. Approximations can be made to synthesize OIS from LIBOR-Fed Funds basis swaps and standard LIBOR swaps, giving you the ability to calibrate the OIS curve, then the LIBOR curve.

Besides the loss of accuracy from approximation, the problem with this approach is your model becomes sensitive to synthetic OIS and not the liquidly traded basis swaps. Because your model is sensitive to synthetic OIS quotes, any deltas you produce to hedge long-dated OIS risks will only be approximate.

Multi-currency Context

The nuances of collateral agreements become increasingly important in a multi-currency environment - particularly for currencies in which there is no native OIS market.

For currencies where there is a native OIS market, domestic instruments can be used to construct the OIS discount curve and the LIBOR projection curves. For instance, domestic OIS and LIBOR curves are first built, then the CSA (credit support annex) discount curves (curve used for discounting in one currency when there is a collateral agreement in another) are constructed by calibrating to cross currency swaps which will have an implicit single currency collateral agreement.

However, if there is no liquid native OIS market like in MXN, then calibration becomes more challenging. Not only are the MXNUSD cross currency swaps collateralized in USD, but the domestic TIIE (Interbank Equilibrium Interest Rate) swaps are as well. The problem is similar to the LIBOR-OIS basis swap issue. We have two sets of instruments dependent on two unknown curves. Domestic TIIE swaps and MXNUSD cross currency basis swaps are both dependent on the MXN discount curve collateralized in USD and the TIIE 28-day projection curve.

An elaborate approximation can be made to synthesize a MXN OIS market; however, this approach is significantly more complicated than synthesizing longer dated OIS swaps in the U.S. market. Also, it makes the determination of portfolio sensitivity with respect to liquid market data unmanageable. Best practice, once again, is to perform dual calibration. This enables you to calibrate directly to liquid instruments without the need for approximations.