For buy side firms, moving to multi-asset investing is becoming critical to adapting to changing markets and achieving a competitive advantage.

A myriad of factors, including difficult market conditions, byzantine global regulations and fierce competition are driving this change. This shift is also placing heavy demands on portfolio and risk systems that were not designed with a multi-asset world in mind.

In a recent webinar, “The Buy Side Evolution: Moving to Multi-Asset,” we explored these trends in some detail. Our lineup of speakers included Kevin McPartland of Greenwich Associates, Marcus Varnai of FINCAD, and Samer Refai of Pension Insurance Corporation (PIC), a $23B institutional asset manager and a FINCAD client.

Kevin kicked off the webinar with Greenwich Associates’ recent research on how the buy side is adapting to increased investor demand for diversified asset allocation. As we all know, the economic environment over the last 5 to 10 years has been nothing short of difficult. The equity markets continue to go up, rates and volatility continue to stay low—and so the search for yield continues.

In speaking to firms about why they want to invest in multi-assets, Kevin said the majority agreed that this strategy provides diversification of the portfolio, helps them to achieve liquidity and lessens volatility. This last area, volatility, is particularly important to pensions and endowments that desire a steady stream of returns to service their liabilities. The least volatility they can have in their returns, the better.

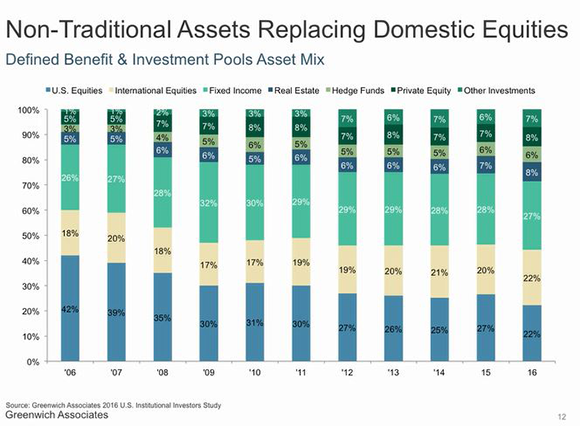

When looking at the non-traditional assets replacing domestic equities in the defined benefit and investment pools asset mix, some interesting trends emerge. Kevin reviewed findings of Greenwich Associates’ global investment management survey that looked back before the crisis in 2006 (as seen on the left side of the diagram below), all the way through to the end of 2016, to see how allocations have changed over time.

Interestingly, the results showed the fixed income portion of the portfolio has remained steady, and really a foundational element in all portfolios. Of course, the instrument, the duration and the yield have inevitably changed over time, as the world we live in today is quite different than in 2006. The research also showed there has been a big overall move away from, primarily, US equities. Many of these assets have been moved to real estate, hedge funds, private equity and other alternative assets, which have increasingly grown in importance. Part of this trend can be attributed to the low yield environment. Firms are searching for yield and are more willing than ever to try new investment types to meet their objectives.

Following Kevin’s presentation, FINCAD’s Marcus Varnai discussed the impact of multi-asset strategies on buy side firms, and covered the benefits of multi-asset portfolio analytics and risk solutions. Marcus explained that the low yield environment means there is increased investor demand for investment performance and diversity. In order to compete with the larger firms, smaller funds need to appeal to their customers by offering a broader range of strategies. They also need to find ways of overcoming competition from robo advisers, and artificial intelligence that are increasingly replacing human investment analysts.

Marcus described that there are now mature solutions in the marketplace that support buy side firms in multi-asset trading. Many tech vendors are working to innovate their offerings to match customer needs, and changing their support and deployment models for these solutions in an effort to make implementation easier. For example, sophisticated valuation and risk solutions like our F3 solution can be up and running in a matter of weeks, giving buy sides flexibility to easily expand into new markets and asset classes as needed. F3 offers a building block approach to product design, meaning you won’t need to recode systems as your needs and the market changes.

Samer Refai of PIC presented the final portion of the webinar, discussing his firm’s requirements for a new Interest Rates and Derivatives desk, and how they built it. A UK insurer focused on defined benefit pension schemes, PIC’s strategy is that of an insurance buy out. Samer works within ALM where he helps manage interest rates, inflation and FX risk on PIC’s balance sheet.

PIC had previously outsourced the execution of hedging trades to an asset manager. However, due to its growing balance sheet size by 2014, the business decided to move that function in-house as it was more economical and increased PIC’s ability to effectively manage risk. This business change resulted in PIC needing a front-office trading and analytics system for derivatives and fixed income instruments.

PIC ultimately selected FINCAD F3. Samer explained they were drawn to the solution because it could be used for live trading, taking in market data and prices for all different types of packages of OTC derivatives and bonds without any interruptions. F3 also provided PIC the ability to model and price a variety of interest rate, inflation, basis, cross-currency swaps and bonds with the flexibility to create non-vanilla structures where needed. Having deployed in 2013, Samer expressed that PIC has been very satisfied with their use of F3, describing it as “fast, accurate and reliable for live pricing.”

For more of what our speakers had to say about buy side firms adapting to multi-asset investing, view our on-demand webinar recording.