Last week my colleague, Russell Goyder, PhD, discussed the Standard Initial Margin Model (SIMM), including three major challenges that firms encounter when calculating initial margin. If you missed the post, check it out, as Russell gives great insight into ways firms can easily overcome SIMM modeling challenges.

This week, I’m picking up on the SIMM topic where Russell left off. But I’ll be looking at it from a slightly different angle. I’ll frame the discussion by touching on some additional highlights from Voltaire’s recent webinar: Derivative Valuation and Margin Calculations.

Specifically I’ll explore some of the key points that Marc-Louis Schmitz, Partner at Finalyse, brought up in his presentation. Interestingly, he looked at SIMM, including initial margin under the EMIR regulation in EU. Below are some highlights.

EMIR Background

In his presentation, Marc-Louis described that following the 2008 crisis, the G20 countries met to discuss the implementation of a regulation that would reduce counterparty risk, improve transparency and mitigate systemic and operational risks. This became known as the European Market Infrastructure Regulation or EMIR. The regulation was intended to help prevent future financial system collapses.

As a result of EMIR, all standardized derivatives must now go through CCP’s. The CCP manages the counterparty risk and takes it on, instead of the market participant or the counterparty being responsible. Another obligation firms have under EMIR is reporting. Every market participant that is trading derivatives needs to send their data to the trade repositories. There is a large amount of data that relates to any given derivatives transaction, which can be hard to manage.

EMIR covers three distinct areas including clearing, reporting and risk mitigation. In the Voltaire presentation, risk mitigation was the main focus of this triad.

Marc-Louis described that when one needs to calculate collateral, there are two types of margin to consider:

- variation margin, which is a payment made to your counterparty on a daily basis to cover the current exposure of derivatives contracts. In the case of OTC derivatives, it should be equal to the positive mark-to-market value, and;

- initial margin, which is a payment made to cover a potential exposure during the time between the last exchange of the variation margin and the liquidation of the position following a default counterparty; typically 10 days with 99% confidence (Note: Initial margin was rarely used prior to EMIR.)

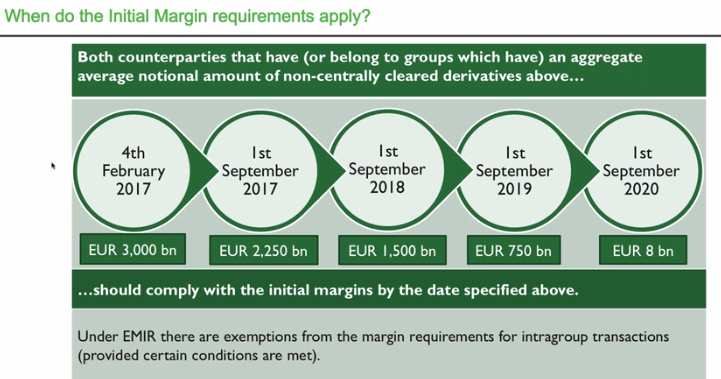

Below is a timeline, courtesy of Finalyse as to when the initial margin requirements go into effect. Depending on the amount of non-centrally cleared derivatives a market participant might have, they will need to adhere to the below schedule. Smaller firms, such as a small life insurers or private bankers, may be subject to the regulation too if they belong to a larger financial institution that is trading derivatives.

Source: Finalyse

Another option firms have is to construct their own initial margin model. The allure here is that margin models can be developed that match up precisely with the exposures a firm actually holds, and account for the sensitivities and covariance within their portfolios, which according to EMIR, need to be based on value at risk (VaR). There are a number of modeling options firms can elect to use here, however some find the development work and obtaining approvals to be a long and costly process.

The best of two worlds?

ISDA SIMM is an attempt to create the best of two worlds—this includes the easy to use, standardized approach of EMIR’s schedule-based method, as well as the benefits that a customized model would bring a firm such as margin that accurately represents their exposures. The newest version was released in 2017. This model is both licensed and maintained by ISDA. Its goal is to promote:

- ease of replication

- better transparency

- good calculation speed

- extendibility to new types of risk, and

- predictable capital allocations.

Many market participants are tending towards the ISDA SIMM Model because of the overall combined benefits it brings. They are assured that the margin will accurately reflect their exposures and they don’t need to worry about model development and governance since this is handled by ISDA. Some calculations show that ISDA SIMM can lead to a substantial decrease in initial margin requirements of up to five times lower.

For more information on how ISDA SIMM works and other SIMM related topics, view the on-demand Voltaire webinar: Derivative Valuation and Margin Calculations