FINCAD recently held a Libor breakfast briefing at the De Nieuwe Poort restaurant in beautiful Amsterdam. The event titled, “Practical Solutions for the €STR, SOFR and SONIA Transition,” was put on in collaboration with organizations, Cardano and TopQuants. I was pleased to learn that the attendees found the presentations informative and the speakers highly knowledgeable on this pressing topic.

David Fletcher, FINCAD’s Managing Director of EMEAI, kicked off the briefing with an introduction on the phase out of the Libor benchmark and what it will mean for affected firms. Certainly, the end of Libor will bring major changes to discount and forward rates in many countries and regions. While, all firms with interest rate exposures will be affected by the change, those that trade in many different currencies and instrument types will feel the greatest impact.

Following the introduction, Jonathan Rosen, Product Manager, Quantitative Analytics at FINCAD, gave a technical presentation on, “Switching to SOFR and SONIA.” He covered three specific areas: curve building, transition hurdles and derivative pricing.

Curve-Building

Jonathan discussed how the changes brought about by the end of Libor affect curve-building and forward rates. He emphasized that the switch to new risk-free rates (RFRs) such as SOFR and SONIA will mean firms need to think about the big changes coming to multi-curve frameworks. “The fact is that Libor will be going away in the very foreseeable future and compounded overnight rates and credit spreads will take its place. If you leave it to the last moment to incorporate these changes, not only may you end up scrambling to modify your existing frameworks, but more sophisticated firms may also be able to take advantage of this. So, it’s prudent to get started right away. I would advise firms to think about their curve-building technology as it stands today. Is it flexible enough to accurately forecast rates through and beyond 2021? If not, consider a possible replacement of your current system to one that is simultaneously built on a modern foundation and fully capable for this transition,” commented Jonathan.

Transition Hurdles

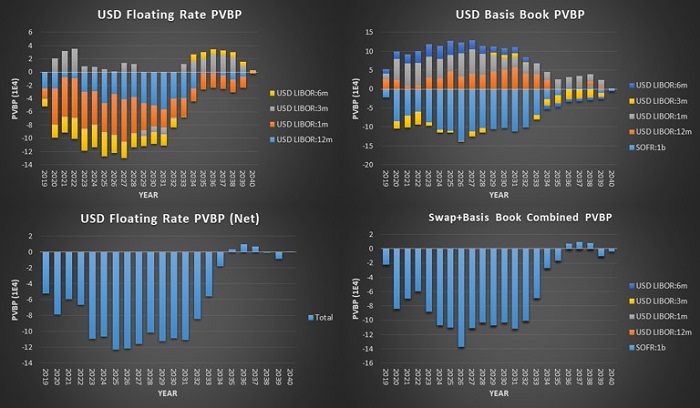

Jonathan went on to explain some of the transition hurdles involved in the move to the new RFR’s. Specifically, he explored the use of the new basis markets between Libor and SOFR/ SONIA, and demonstrated how they can be used to hasten the transition for delta-1 products. One example Jonathan gave is illustrated in the chart below.

The graph on the upper left shows a USD swap book with around 800 swaps, with Libor exposure at multiple tenors from 1m to 12m. The fixing risk is displayed in PVBP buckets by year. Shown in the upper right graph is a basis book, with Libor exposure at multiple tenors and also SOFR exposure.

Moving down to the graph in the lower left, we see a comparison of the net floating rate PVBPs of the original book. On the lower right, we see the pure SOFR PVBPs once the two books have been combined. Interestingly, the total DV01 is nearly the same within a fraction of a percent, and the bucketed PVBPs are similar with only minor differences due to switching from forward-looking to backward-looking rates. Overall the rate risk is extremely well preserved. Jonathan remarked that benefits of this approach include the control over the timing of Libor transition, the choice of spread profile and avoiding unexpected valuation impacts in the coming days.

Derivative Pricing

In the final portion of his presentation, Jonathan discussed some of the big and unresolved challenges that still exist for non-linear products on Libor. A major issue with these products is that it’s not even clear how a transition will happen and what sort of fallbacks will be used for options and exotics. He noted this is something there has been little to no guidance on from bodies like the ARRC, and which he believes deserves attention in order to give market participants more clarity.

Transitioning from EONIA/EURIBOR to €STR

Attendees of our briefing then heard from guest speaker Max Verheijen, Managing Director at Cardano, who discussed the transition from EONIA/EURIBOR to €STR. Max gave a timeline for the events leading up to the switch to €STR discounting. He also explored the practical implications from the changes to €STR and what the potential fate will be for Euribor. Lastly, Max put forth a useful summary of steps firms can take leading up to the €STR transition, which can help ensure they are well prepared for the change once the 2021 deadline hits. As one might expect, a lot of the preparation work will involve ensuring firms’ systems are ready and able to cope with €STR.

If you are interested in attending one of FINCAD’s live events on the Libor transition or other topics in derivatives and finance, check our Events Webpage. Here you will find a listing of our current events and links to register. For more on Libor, watch our brief videos:

The End of Libor: Time for Action

Overcoming the Top 5 Challenges of the Libor Transition