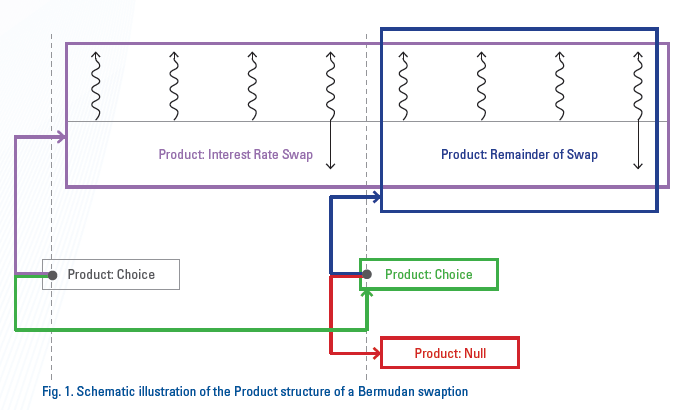

In my last post, I covered some useful specializations of the idea of a Product, but this is far from an exhaustive list. We could keep going, constructing higher-level structures such as that of the Bermudan swaption from Part 5, but this just amounts to further convenience; each such structure conforms to the definition of a Product and can be constructed using the above building blocks.

{kind=link}

So far, we have made the tacit assumption that Flows are cash flows - measured in units of currency, not some other asset. However, everything we have said applies equally well to cash-settled and physically settled trades alike. There is one area, however where the distinction matters. From the point of view of valuation, the obligation to make a cash payment has value as long as it has not yet occurred. Flows made in the past do not contribute to the value of a derivative. In order to continue to reflect the value of cash received in a given Flow, it is most natural, from the point of view of a derivative valuation system, to invest that cash in another vehicle such as a cash deposit where our counterparty is obliged to make a cash payment to us in the future. Cash has value by virtue of it being promised to us in the future - this is a fundamental tenet of derivative valuation.

But what about the underlyings from which derivatives are derived? Typical portfolios contain both securities and derivatives and any generic system needs to accommodate both. For the receipt of securities - flows of physical assets such as bonds, stocks or commodities, where the receipt of such assets reflects their ongoing ownership, we need to account for them differently. We do this by drawing a distinction between cash and physical securities. For the latter group, we can construct the following structure.

Consider a simple bond trade. It is best described as a Swap consisting of two Flows, one of cash (the agreed price of the bond) and the other physically settled (representing receipt of the bond itself). Before the trade is settled, its value is the present value of the difference between the forward price of the bond and the fixed payment to be made for it. After settlement, the value is that of the then market price of the bond.

This may seem a trivial point, but failure to capture it can lead to significant confusion when calculating the value and exposure (in all its forms) of realistic portfolios.

That's it for Products in this series. So far we have focused exclusively on encoding the rights and obligations expressed in a term sheet. We have been talking about what is valued, but have said nothing about how it might be valued - in the context of some model and valuation methodology. I'll venture into the realm of modeling in my next post.