For investors looking to diversify their portfolios with potentially lower risk, municipal (muni) bonds are becoming an increasingly attractive investment option. In this blog, we explain how muni bond investors can use swaps to hedge their exposure to interest rate fluctuations and inflation expectations, which have been the main drivers of muni bond market performance in 2024. We also show how FINCAD Analytics Suite from Numerix can help muni bond investors price and risk manage their bonds and swaps in a consistent and reliable manner.

Assessing the Risks

A main source of market risk for muni bond investors is interest rate risk, which arises from the inverse relationship between bond prices and interest rates. When interest rates rise, bond prices fall, and vice versa. Inflation risk is another source of market risk affecting muni bond investors, which occurs when the purchasing power of money declines over time due to the general increase in the prices of goods and services. Inflation reduces the real value of future cash flows from bonds, leading to lower returns for investors.

Hedging

One way that muni bond investors can hedge against interest rate and inflation risk is by using interest rate and inflation swaps, which are derivative contracts that allow two parties to exchange interest payments based on a notional principal amount. As an example, by using interest rate swaps, muni bond investors can effectively convert their fixed-rate receivables into variable-rate payments that are linked to a market index, such as SIFMA or SOFR.

It’s worth highlighting that when hedging, fixed rate investors pay fixed and receive float. This way, if interest rates and inflation rise, investors will receive higher payments from the floating leg of the swap, which will offset the lower value of their bonds. Conversely, if interest rates fall, investors will receive lower payments from the floating leg in the swap, but their bonds will increase in value.

When encountering other interest rate exposures, such as receiving a floating bond coupon, investors may enter into an interest rate swap in order to receive a fixed coupon and hedge against a declining interest rate. Thus, swaps can help muni bond investors reduce their interest rate and inflation risk and protect their portfolio value.

However, entering into swaps also involves some challenges, such as finding a suitable counterparty, negotiating the terms of the contract, and managing the collateral and counterparty risk. Moreover, swaps require sophisticated valuation and risk management tools, as they are complex and customized instruments that depend on various factors, such as market conventions, interest rate indices, and swap structures. To help understand the impact these different factors have on the price and the cashflows of a swap, it helps to analyze some initial assumptions and see the impact.

Simplifying Muni Bond Investing

FINCAD Analytics Suite for Excel is a powerful, flexible tool that supports the diverse and evolving needs of the muni bond market. Key solution highlights include:

- Easy calculation of key metrics for muni bond portfolios, including yield, convexity, cash flows, option values, and risk sensitivities, such as DV01 and duration

- Comprehensive coverage for muni bond valuation models, including tax-adjusted discounting, option-adjusted spread, and binomial tree methods

- Support for various types of muni bonds, such as general obligation, revenue, pre-refunded, callable, puttable, and convertible bonds

- Ability to define customized payoffs, incorporate curve or market data scenarios, carry out par rate or yield analysis for a series of bonds, perform forward valuation scenarios, and observe historical basis to relevant benchmarks

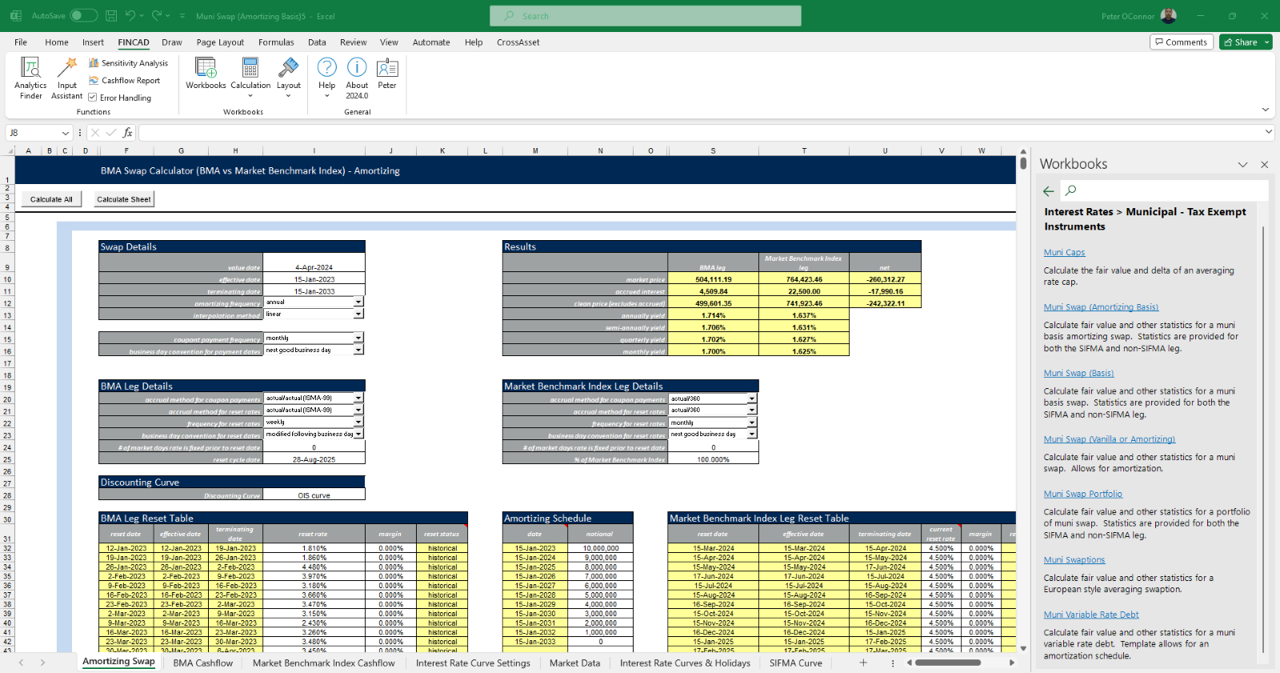

Shown above: Swap pricing product workbook with pricing, risk and projected cashflow analytics

FINCAD Analytics Suite from Numerix elegantly handles complex and customized swap structures, such as floating-to-floating, amortizing, accreting, step-up, inflation and basis swaps. Investors can be confident that different market conventions are accounted for, such as day count, compounding, and payment frequency, as well as various interest rate indices, such as FedFunds, SOFR, and SIFMA. Evaluating the fair value, sensitivity, and risk profile of swaps, as well as performing scenario analysis, stress testing, and hedge effectiveness assessment are all simplified using the solution. Plus, FINCAD Analytics Suite empowers investors to measure and manage their exposure to counterparty credit risk and collateral requirements.

Recapping our Muni Bond Recommendations

There is growing appeal in muni bonds as a diversification strategy for investors seeking lower risk. Swaps can be used to mitigate the main risks facing muni bond investors, namely interest rate and inflation risks. However, navigating the complexities of swaps involves challenges such as finding suitable counterparties and employing sophisticated valuation and risk management tools. Through solutions like FINCAD Analytics Suite, muni bond investors can effectively price, manage risks, and simplify their investment strategies, despite the complexities involved in swaps and market conventions.

FREE Trial: FINCAD Analytics Suite

Would you like to begin gaining deeper insight into the performance and risk of your muni bond portfolio? Get started today. We’d like to extend you the opportunity to try FINCAD Analytics Suite for Excel free for 14 days. Experience how easy it is to value and risk manage muni bonds and swaps in a consistent and reliable way using our award-winning analytics library.