The Standard Initial Margin Model (SIMM), produced by ISDA, provides a methodology for the calculation of initial margin (IM) for uncleared swaps that complies with margin requirements for non-centrally cleared OTC derivatives in the US, European Union (EU), and Japan. The aim of SIMM has been to reduce the number of disputes over margin calculations.

Voltaire Advisors recently hosted a webinar titled, “Derivatives Valuation and Margin Calculations” to help industry professionals understand issues and their options when it comes to managing SIMM. Speakers included: myself, Ian Blance, Managing Director at Voltaire Advisors and Marc-Louise Schmitz, Partner at FinAnalyse.

Some SIMM History…

SIMM was originally introduced by the International Swaps Dealer Association (ISDA) in 2013 as a response to the financial crisis; and in particular a response to the Basel committee/IOSCO consultation paper that was released in 2008. The paper looked at ways to reduce systemic risk in the derivatives market and suggested margin requirements for non-centrally cleared OTC derivatives.

In essence, SIMM has been designed to mitigate systematic risk and create a global collateral margining framework that will lead to greater transparency and less disputes. Version 1.0 of SIMM went live in 2016. However, the ISDA periodically reassesses and recalibrates SIMM risk factors in order to meet regulatory standards and market conditions. Thus, version 2.0 was just released in December 2017.

There are a number of challenges firms are encountering with regard to SIMM. Implementation of the SIMM calculation itself is pretty straightforward. You can code it yourself, get a vendor solution or leverage one of the open-source implementations that are available. So this is not a very big deal by design. Even the updates to SIMM are fairly infrequent and relatively easy to manage.

However, the other main input to the SIMM model is standardized sensitivities. This requires fast and accurate valuation calculation for derivatives. It’s worth noting that SIMM is standard only up to the sensitivities that it consumes. So, SIMM calculation is really won and lost in the sensitivities. These calculations are the limiting factor in the quality and timeliness of the resulting initial margin numbers.

The Challenges

In my presentation, I focused on three challenges –each of which relates to sensitivity calculation. These included:

1. Speed of Sensitivity Calculation: Calculation speed is important in minimizing initial margin through selection of counterparty, pre-trade, for example. But this really applies to any pre-trade analysis that involves margin, such as calculating all-in par rate or running spread for a deal. These require immediate turnaround of margin calculations.

However, typically finite difference calculations use the “bump and grind” or “bumping” method. This is where we make a small change or perturbation to a quote or quotes and then revalue. This can be expensive because in addition to revaluing, you need to recalibrate. Plus the more quotes we have that feed our curve build and model calibrations for the valuations, the slower the calculation will be. The end result of this is that risk management is an overnight activity as opposed to an intra-day or pre-trade one.

Some firms will throw hardware at the problem. But this can be costly to setup and manage, requiring either new hardware installation or cloud bandwidth. And we are still operating within the same paradigm –a turtle is still a turtle (slow) even if you strap a rocket to its back.

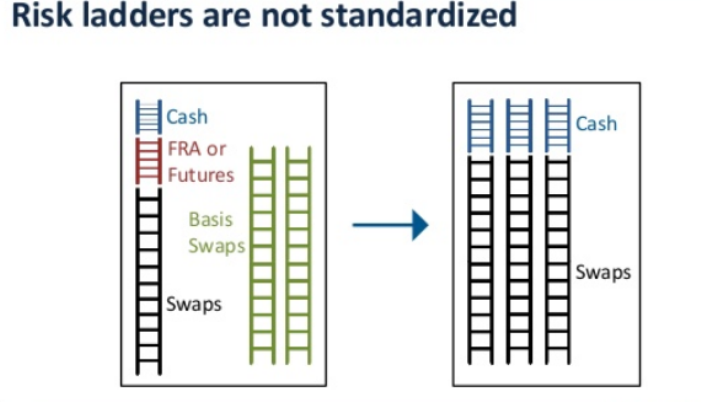

2. Standardized Sensitivities: The second challenge I spoke about is how SIMM’s standardized risk factors do not always map exactly to the reality of the derivatives pricing model. That is, you must decompose your netting sets into the standardized risk factors.

As an example, it is very common for interest rate curves to be built using futures and basis swaps. And yet these instruments do not appear in the standardized risk factors that correspond to standardized instruments for driving SIMM, which would be cash deposits and vanilla swaps. So you end up having to price those standard instruments in your pricing model in order to generate essentially a different model, which is the one that will be bumped to get the required sensitivities. This is cumbersome to set up, slow to run and it introduces an inconsistency between your pricing model and your margin model.

3. Portfolio and Netting Sets: The third challenge I explored in my presentation is how difficult it is calculating sensitivities consistently across a portfolio. Everything I’ve said above assumes that we have a pricing capability that covers all of the derivatives in each of our netting sets. To achieve that coverage, it is fairly common to see firms using a patchwork of in-house and vendor libraries and spreadsheets often accumulated over a decade’s time. The more heterogeneity you have in your analytics ecosystem, the harder it is to standardize. And of course standardization is the name of the game when it comes to SIMM. Thus, standardization across portfolios and portfolio level analysis of valuation and sensitivities becomes costly to set up. Plus, internal arbitrage can creep in whenever you have the same thing modeled in a slightly different way in different pricers.

An Answer to the Problem

To address the above challenges, my recommendation is to utilize the mathematical technique, algorithmic differentiation (AD). AD is a modern solution to the problem of fast and accurate sensitivity calculation. The beauty of AD is that it is staggeringly fast. Typical speed-ups over bumping are in the hundreds or thousands of times faster.

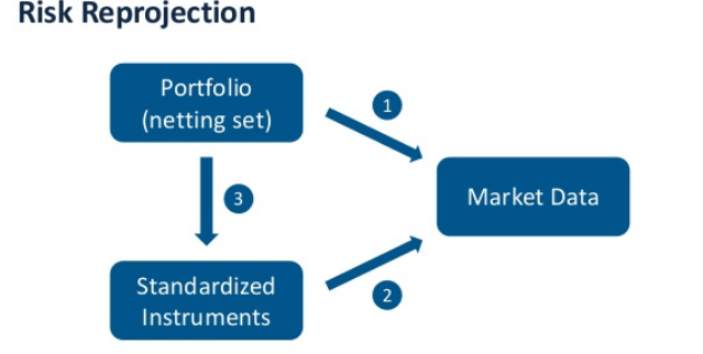

AD gives you fast sensitivities. But for SIMM you also need standardized sensitivities. This can be achieved through the technique of risk reprojection. How it works is that risk reprojection combines the market sensitivities of your netting set with the market sensitivities of the standardized instruments that define the standardized risk factors. Those sensitivities are then tied to the same market data (as seen in the diagram below), or the inputs to the pricing model. What we are ultimately after is the sensitivities of our netting set to the standardized instruments.

Risk reprojection works in a similar way in calculating a cross-rate in FX. Except instead of dividing one number by another, we end up having to divide vector of sensitivities (shown in arrow 1) by a matrix of sensitivities (shown in arrow 2). This can be done with the standard technique of linear regression.

Risk reprojection avoids the cumbersome steps of synthesizing market data. By operating with the sensitivities that you have it pairs quite nicely with AD. Thus the whole calculation can be done in one fast step and within one modeling context.

If you are interested in more details on this topic, view the full on demand-webinar: Derivatives Valuation and Margin Calculations.” In it, you’ll find extended examples and information on the key role an integrated portfolio and risk analytics platform plays in helping firms cope with SIMM.