The economic environment over the last several years has been nothing short of complicated. The equity markets continue to go up, rates and volatility continue to stay low—and so the search for yield continues. These trends are making multi-asset investing an increasingly attractive option for buy side institutions.

However, often deploying multi-asset strategies is not as simple a task as it ought to be. One of the biggest challenges relates to technology. Firms are finding that diversifying their portfolios places heavy demands on their portfolio and risk systems, which were simply not designed with a multi-asset world in mind.

At FINCAD, we’re involved daily with buy side firms that are endeavouring to solve a range of software challenges related to multi-asset investing. The following example is based on an experience we had helping one our clients. Names have been changed to protect the innocent. ;)

The Situation:

Ian is the CIO at a leading asset management firm. It has been a good quarter so far. However, their customers are looking for more diversity for their investments, and there is pressure to keep up with the range of investment opportunities offered by the competition.

The firm is hiring with a plan to launch new funds with an emerging market focus and a mandate that includes FX equity and rate hybrids. Ian needs to work with the other teams to ensure they have all the necessary support systems in place.

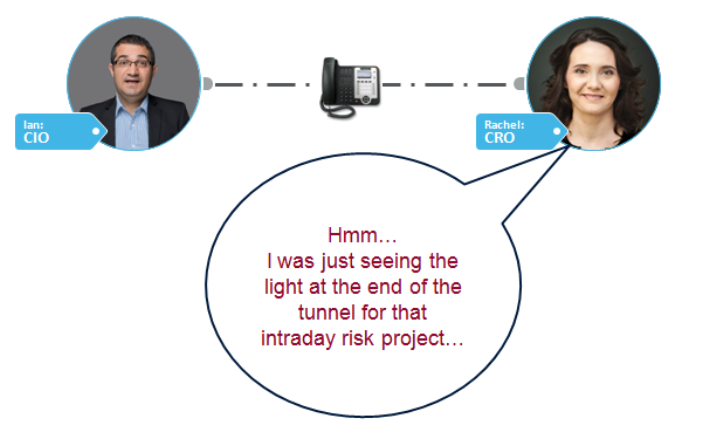

Ian calls Rachel in Risk to discuss what will be needed. Rachel has been working hard on a project to get risk intraday for the existing funds, and is concerned that this new effort will distract from that effort.

Rachel proceeds to call the CTO, Tina, to discuss the system requirements to support trading, risk management, and reporting for the expanding business. Rachel wants to be able to monitor risk intraday, for the new funds as well. Plus, the expansion of geographies and asset classes means new regulatory reporting requirements too.

Tina explains that they will need to speak to Alan, the desk quant analyst, to get to the bottom of product coverage and analytics in the first place. There will likely be problems with the emerging markets product conventions. Rachel is now feeling less confident, and adds Alan to the call.

Alan had a heads up about this already, but he needs to do further research on the product and curve building conventions in these geographies. He reminds Tina that they don’t have market or reference data sourced for these markets yet either.

Alan mentioned that he checked the available versions of their existing systems and is certain that the current analytics library will not cover what they are planning to invest in within these markets. Therefore, he has started writing some bespoke pricers behind Excel as a potential stopgap.

The Challenge:

Alan becomes stressed. His spreadsheet pricers are coming apart at the seams. The firm’s vendor can add the market conventions he needs, but not until the next product release. That means it will be six months before they can start the upgrade.

The best the vendor can do is pull numbers together from the bespoke pricers and their other internal systems to build the most critical reporting intraday, then do a sanity check daily with risk measurements from their hosted risk service.

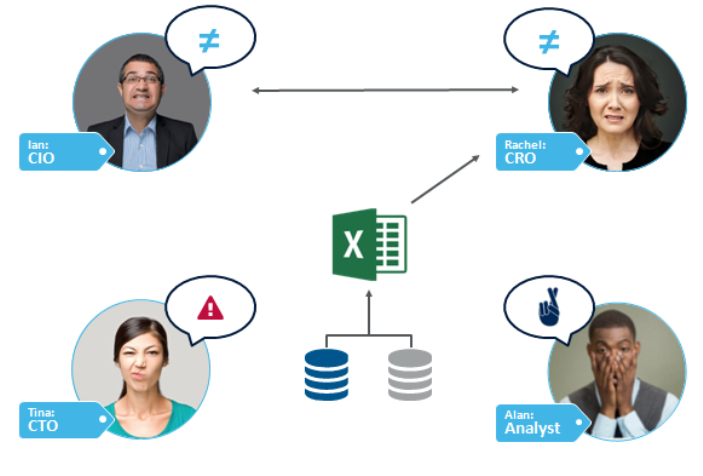

Rachel, the CRO, is concerned because for all the manual work Alan has to do, she can still only get comprehensive risk and P&L for all the funds on a delayed basis. She is quite worried about the operational risk created by spreadsheets and manual workarounds. Ian wishes that he and Rachel did not spend most of their time trying to understand the differences between the middle and front office view of risk and P&L.

Rachel, the CRO, is concerned because for all the manual work Alan has to do, she can still only get comprehensive risk and P&L for all the funds on a delayed basis. She is quite worried about the operational risk created by spreadsheets and manual workarounds. Ian wishes that he and Rachel did not spend most of their time trying to understand the differences between the middle and front office view of risk and P&L.

The risk and trading teams can’t get accurate, timely information. A lot of time is wasted on reconciliations— and there is a large amount of operational risk.

The Solution:

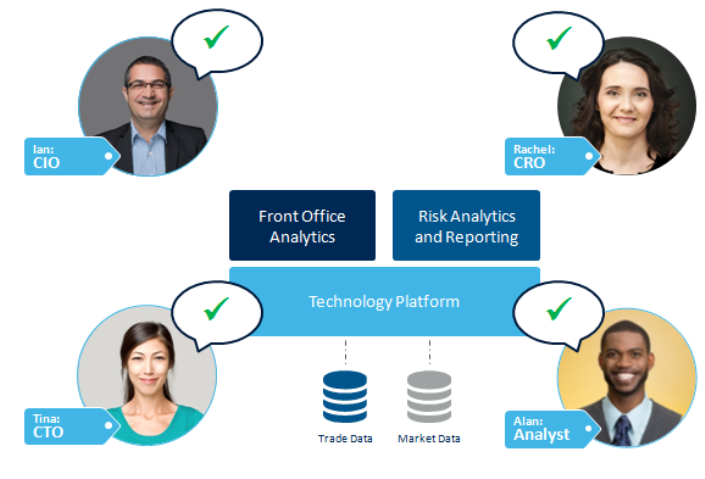

After a review of portfolio and risk systems, the team elects to implement a core valuation and risk solution integrated with best-of-breed order management systems and back office services.

As a result, Ian now has the pricing and risk analytics that the trading team needs, and the flexibility to enter new markets and new asset classes as business needs demand. Everyone works from the same market data and curves, so Rachel and Ian spend their time optimizing the business, rather than reconciling P&L and risk.

Rachel now has reporting consistency and can get risk and P&L on-demand. The system also generates many values she needs for regulatory reporting.

Rachel now has reporting consistency and can get risk and P&L on-demand. The system also generates many values she needs for regulatory reporting.

Alan has access to pre-configured market definitions for all major currencies, with the flexibility to customize the methodology if he needs to, and the support to extend the valuation environment for new markets to keep up with business demands.

The new system is built on a robust and open technology platform, which makes it easy to integrate with other best of breed solutions. The operational risks have been removed and there is vendor support going forward for any further expansion.

Simplify Multi-Asset Investing

The scenario above is not an uncommon one for many of the firms we work with. The reality is that now there are more asset types than ever that need to be managed and risk managed, thus technology that has been designed specifically to support multi-asset portfolios is critical. Using such systems is the only way firms will gain the freedom and flexibility they need to expand into new asset classes and products quickly and painlessly.

To learn more about this topic view our on-demand webinar: The Buy Side Move to Multi-Asset Trading