In just a few short weeks, the coronavirus has wreaked havoc on our daily lives and the global economy. Market volatility has increased dramatically, mostly due to significant declines, but also due to some recent positive swings.

In just a few short weeks, the coronavirus has wreaked havoc on our daily lives and the global economy. Market volatility has increased dramatically, mostly due to significant declines, but also due to some recent positive swings.

Drastic measures are now being taken to combat the spread of this novel virus. With investors reacting to the latest news of government stimulus, community infection rates, and expert opinions from all corners, we are on track to face further surprises in the markets over the days ahead.

Over the past year, we have had a prolonged span of low volatility, shown by the VIX ceiling of low twenties. Yet, as of just two weeks ago, it has reached a peak of around 83, and since then has remained elevated. VIX is currently sitting above 60 and is likely to stay high as long as there continues to be uncertainty surrounding COVID-19 response effectiveness, and until the wider economic impacts of this situation materialize.

Many investors are struggling to come to grips with the market’s sudden switch to high volatility. This has had widespread implications not only for current price behavior, but also for vega-sensitive positions. Some hedge funds that trade volatility have already shown the severe impacts of this regime change, even resulting in their sudden collapse. Still other firms that have net long vega positions are likely to have reaped some benefits from this new environment.

Now that high volatility is here, it is natural to wonder how long it will last. The reality is that no one knows for certain what the days ahead will look like. Facing the possibility of continued high volatility, firms will need to consider taking steps to limit their downside risk as markets continue to search for a bottom. However, if the market does reach equilibrium despite the price declines, this may also lead to volatility trending back closer to historical norms. Shifting to short vega positions could pay off if the current situation stabilizes.

There are many different approaches to shorting vega with options. In the current situation, where there are still some price swings to come followed by price stabilization, a long-gamma/short-vega strategy, such as a calendar spread, could make sense. By buying short-term and selling long-term ATM options, you are simultaneously positioned to profit from current price movements, as well as future reductions in implied volatility.

However, there are some caveats to calendar spreads. Among these are the fact that they are not delta neutral, so by choosing call or put spreads you are effectively biasing the break-even price movement up or down. Another thing to watch out for is the timing of this strategy, as the short-dated option is responsible for the net long gamma. Therefore, holding this strategy through the first expiry will end up in an ordinary short option position with negative gamma.

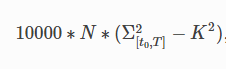

Rather than worry about the delta and gamma risks inherent to calendar spread strategies, it may be more beneficial to have a position that is purely sensitive to volatility, and not the underlying price. An option that can work here is the variance swap, which pays the difference between realized and implied variance over a given time span. The terminal payoff is the following:

for notional N, realized volatility Σ[to,T] and strike K. Given the initial strike level depends on the level of implied volatility, variance swaps provide a convenient way to take positions purely in terms of volatility. Thus, they may be an ideal tool for any volatility swings ahead, either as a hedge or more as speculation.

for notional N, realized volatility Σ[to,T] and strike K. Given the initial strike level depends on the level of implied volatility, variance swaps provide a convenient way to take positions purely in terms of volatility. Thus, they may be an ideal tool for any volatility swings ahead, either as a hedge or more as speculation.

FINCAD provides complete analytics for the valuation and risk management of a wide range of volatility derivatives from vanilla to exotic. Hundreds of firms rely on FINCAD to help future-proof their businesses against uncertainty like we are seeing with COVID-19. Look out for our future article where we will go into depth on the different types of variance swaps with examples of how they performed in the recent market upheaval.