Mortgage-backed securities (MBS) are increasingly falling into favor with today’s investors. The appeal with this structured credit product is that it offers a potentially better payoff than vanilla instruments. However, the flip side is there may be greater risk involved. Thus, in terms of investing, one needs to evaluate the risk/reward profile and determine if MBS is a good fit for their firm’s overall investment strategy.

MBS 101

MBS are pools of retail mortgages that are bundled up and sold as securities by government agencies such as, in the US, Freddie Mac or Fannie Mae. MBS have generated fairly good long-term returns. In fact, through June 30, 2013, the Barclays GNMA Index had generated a 10-year average annual total return of 4.78%, in line with the 4.52% return of the broader US investment grade bond market. In a September 2019 report of the US MBS market, Invesco reported the current yield of MBS at 4.5%.

An Example: Pass-Through MBS

A pass-through is perhaps the simplest form of MBS. How technically does it work? Let’s explore the diagram below.

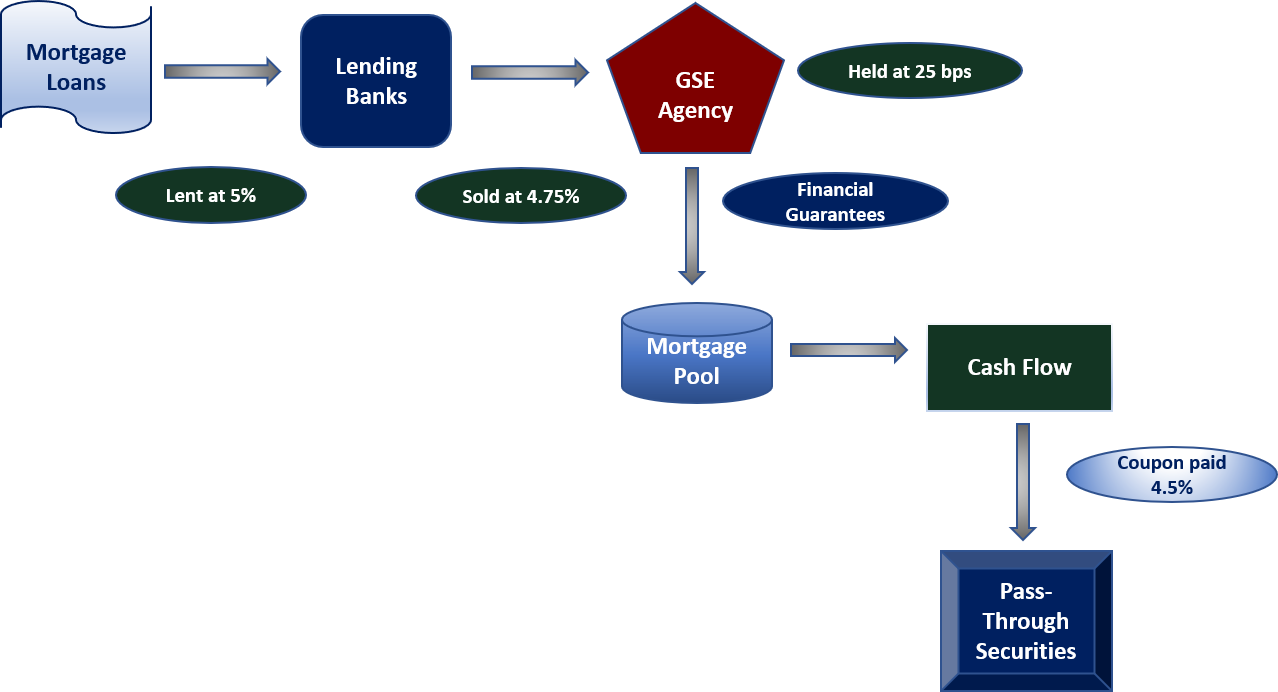

For the purpose of this example, we start with a group of retail mortgages at the fixed interest rate of 5%. In the US, the lender would sell these mortgages to a government-sponsored enterprise (GSE) like Freddie Mac or Fannie Mae at a lesser rate of 4.75%. There would be a spread in this transaction in terms of the profit for the lender. After the purchase, the GSE retains the pool of mortgages.

From there, securities are issued by the GSE that pass through the cash flows to the investors. There is a difference in interest rates that are paid on the mortgage collateral pool and the actual coupon on the pass-through securities. In the above example, it is 4.5%. This is referred to as a servicing spread, which is intended to cover the cost of collecting and distributing the cash flows.

In this example, the servicing spread is 25bps, which results in a net pass-through coupon of 4.5%. One advantage of these “agency securities” is the financial guarantee offered by the GSE. Thus, if a mortgage borrower defaults in the underlying pool, the GSE will make up the principal shortfall to the pass-through investors. This effectively removes credit risk from agency MBS investing.

MBS Challenges

One of the major challenges of incorporating MBS into an investment strategy relates to modeling. Because MBS are a complex investment type, they require very specialized modeling considerations.

For example, the range of possible MBS tranching decisions can create many different payoff profiles. Thus, without a flexible modeling framework, investors will struggle with both projecting cash flows and performing valuation and risk calculations.

Effective MBS Modeling

The modeling challenges of MBS can be overcome using a generic, modular approach to MBS analytics. This is exactly the approach that is taken in our FINCAD F3 solution. With F3, users get access to a highly flexible MBS analytics framework. They are able to identify the fundamental concepts in their analysis workflow. From there, they use these concepts as building blocks that combine to form a complete MBS analytics system.

This MBS framework design is generic and flexible enough to support any kind of MBS analysis that you want to carry out. Each module in the framework can be swapped out and replaced as desired, without affecting the other parts of the system.

In addition, with F3, support for the definition and cash flow generation of pass-through securities is handled natively. It’s important to note that the universe of cash flow waterfall structures is vast and there are numerous ways that tranches can depend on each other in a deal. For this reason, in the F3 analytics library, there is the option to easily specify a tranche by supplying a security identifier such as CUSIP/ISIN. FINCAD has partnered with leading data analytics providers, Andrew Davidson & Co., Inc. and Intex, to offer this functionality.

Consistency is Key

It’s important to remember that there is no single gold standard model that should be used for modeling MBS. What’s most vital is not the model you pick, but whether you are using the same modeling framework consistently across all securities in your portfolio. And, in fact, FINCAD F3 offers users one modeling framework and set of assumptions that can be used across all the assets in your portfolio. This consistency is invaluable to your success with modeling MBS.

Read more about MBS modeling here: Building an Effective MBS Analytics Framework for Valuation and Risk