Preparing your option pricing and risk models for negative commodity futures prices

This week began with a shocking decline in the May WTI oil futures contract price. In an unexpected sequence of events, combining the low demand for oil, a definitive lack of storage options, and a rush of traders exiting positions before delivery obligations were to occur, the perfect storm was created. The WTI May contract price was sent into negative territory, to a low of around $38. This event has left investors stunned and faced with the difficult question of how to adjust their pricing and risk models to cope.

Previously, it wasn't even regarded as a possibility that oil futures contracts could reach zero, let alone turn negative. Nevertheless, the virtual “impossible” happened, and the result has been general confusion. Interestingly, the negative dip was less of a widespread phenomenon than many realized. It was due more to the localized phenomenon of oversupply, low demand and storage availability at the WTI delivery site in Cushing, Oklahoma.

While we shouldn't expect gas prices to turn negative at the pump anytime soon, this does point to the possibility that crude oil futures can turn negative under extreme circumstances. This is something that is only now being viewed as a legitimate concern for commodity investors.

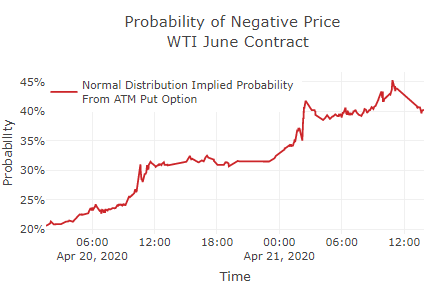

And so, now that the May contract has settled into delivery, the question turns to June. Large price swings mean that the implied volatility for the June futures contract options has increased dramatically. If we use a model that allows negative prices, such as the normal model, and compute the market-implied probability of prices at or below zero until settlement, we can see at left that the possibility of negative prices under this model is rapidly increasing to levels of 40-50%. This model shows there is a clear expectation of negative prices in the June contract as well, due to recent events and accompanying increases in contract price volatility.

And so, now that the May contract has settled into delivery, the question turns to June. Large price swings mean that the implied volatility for the June futures contract options has increased dramatically. If we use a model that allows negative prices, such as the normal model, and compute the market-implied probability of prices at or below zero until settlement, we can see at left that the possibility of negative prices under this model is rapidly increasing to levels of 40-50%. This model shows there is a clear expectation of negative prices in the June contract as well, due to recent events and accompanying increases in contract price volatility.

Back in 2014, we saw a similar situation occur for interest rates, with short-term deposit rates at a number of European central banks turning negative. This was a more widespread issue due to the importance of interest rates in most asset classes, and in particular, for interest-rate options there were many technical challenges. The widespread use of the Black-Scholes option pricing model is an important question for negative rates, due to the fact it is built on a geometric Brownian motion which requires the underlying remain strictly positive. When interest rates turned negative, many found that their option pricing models no longer worked, presenting serious challenges for pricing and risk management activities like delta-hedging.

Now that a similar situation has occurred for WTI futures, it is worth considering how to move beyond the Black-Scholes model for WTI futures options. As mentioned above, one of the first models that comes to mind for negative values is the normal model. While switching to the normal model is certainly one way to accommodate the possibility of negative prices, it is also a rather extreme change to the model dynamics. It may be reasonable to believe that the true estimate of the negative price probability is significantly less than what what the normal model describes. And, furthermore the switch to the normal model would have a dramatic impact on hedging strategies by changing the option delta. Beyond this, the use of normal model implied volatilities could have a significant impact on the construction of implied volatility surfaces.

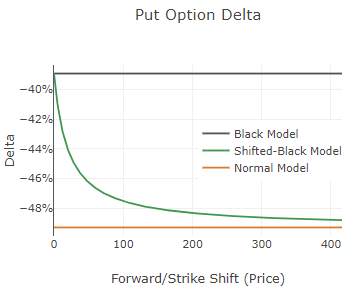

One alternative to the normal model is the shifted-Black model. As shown at right, the option delta of the shifted-Black model lies somewhere between the Black model and the normal model. As the shift that is applied to the forward and strike in this model is increased, we can see behavior increasingly similar to the normal model. However, at more modest levels of the shift, the shifted-Black model remains similar to the Black model and tends to be less of an extreme change from this trusted option pricing model.

One alternative to the normal model is the shifted-Black model. As shown at right, the option delta of the shifted-Black model lies somewhere between the Black model and the normal model. As the shift that is applied to the forward and strike in this model is increased, we can see behavior increasingly similar to the normal model. However, at more modest levels of the shift, the shifted-Black model remains similar to the Black model and tends to be less of an extreme change from this trusted option pricing model.

If you are concerned about the possibility of negative futures prices in the WTI or other commodities, it may be a good time to rethink your use of Black-Scholes for these option contracts. Rather than switch to the normal model, you may benefit from using a shifted-Black model, which does not depart as extremely from the behavior of Black-Scholes in terms of hedging and volatility surface construction.

By determining an effective floor on the level of the underlying futures contract and using this as an estimate of the shift needed in the shifted-Black model for later contracts, you can take the necessary steps to future-proof your models for the real possibility of negative futures prices–all without causing too much disruption to your current strategies.