In a recent webinar, FINCAD and TP ICAP brought together their collective experience in helping firms optimally navigate the Libor transition. “A Look Inside the Libor Transition: Combining High Quality Market Data and Powerful Financial Analytics,” featured speakers, Irina Orlova, CFA, Senior Product Manager, Risk at TP ICAP Data Analytics, and Jonathan Rosen, PhD, Product Manager, Quantitative Analytics at FINCAD. The presenters walked through how firms can achieve a successful transition off the retiring Libor benchmark rate by leveraging high quality data and robust analytics.

Below are three key takeaways from the event:

1. Don’t Wait, Take Action Now!

You can’t begin too soon preparing for the Libor transition. In fact, it is only to your advantage to begin reducing your exposure to the Libor benchmarks immediately.

So, how does one get started? First, take a good look at the scope of your current exposure to Libor, as it may be present in various business lines throughout your organization. You can then examine the ISDA Libor fallback protocol contract amendments to work through what your potential impact might be.

A good course of action is to incorporate Libor fallbacks into all your existing and new deals to prepare for Libor cessation. If possible, work to decrease your Libor-linked investments and ramp up Libor-free strategies across all business areas. Fortunately, FINCAD clients are able to take advantage of FINCAD algorithms that help them determine the trades required to offset any Libor-linked obligations.

It’s also worth noting that certain instrument types can be easier to transition than others. For example, portfolios containing derivatives instruments that rely on Libor can be taken care of easily, as the OTC derivatives market is very flexible and less heavy lifting is therefore needed to transition to new RFR’s. However, if your portfolio is heavy on loans, floating-rate bonds, or other credit-structures, the negotiation of the contracts may be more time-consuming, especially if you do not choose to automatically incorporate the fallback rates. It is critically important to factor the time investment needed for transitioning your different instrument types.

2. Anticipate Changes

As we head into the Libor transition in 12-18 months, it will be crucial to start accounting for a combination of historical fixings, curve instrument market data and modeling analytics, which are required to price things like legacy Libor trades after the benchmark disappears. We also need to account for the newer alternative rate instruments such as those based on SOFR and ESTR.

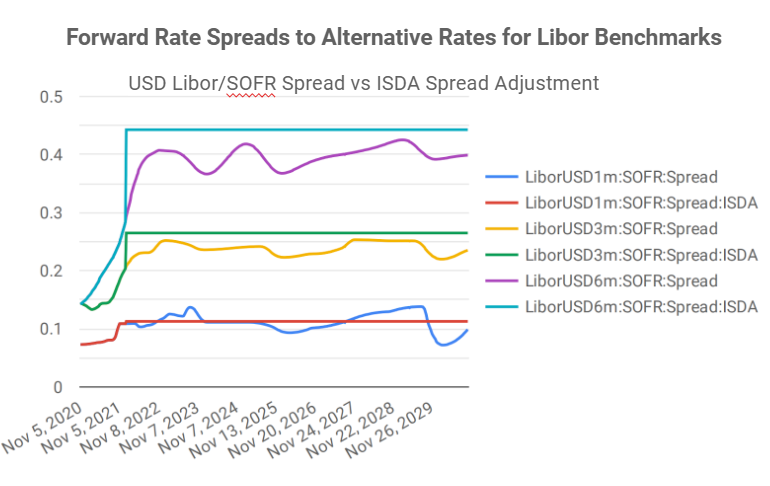

Soon we will also be faced with the question of adherence to the ISDA protocol for Libor fallbacks. Composed of both an alternative rate benchmark and 5-year historical median spread adjustment, the ISDA fallback involves geometric compounding in arrears for both historical fixings, as well as points on the modeled alternative rate forward curve.

For the new crop of instruments, there could also be several alternative calculation types to be aware of, including in advance compounding and features like lookbacks, payment delays and others, that may be found in the various instruments.

In order to accommodate all these details, a number of curve features are usually required. These may consist of, but are not limited to, spread-based construction, (which mimics the internal relationship of the ISDA fallback), central bank meeting dates, as well as a flexible choice of instruments to accommodate market data changes. Other features might include the need for global calibration, which gives you the ability to calibrate interconnected curves. This feature can be particularly important for the liquid basis swap markets.

3. Quality Data and Analytics are Invaluable

High-quality market data for alternative rates is a must-have for the Libor transition, especially with the reliance on actual transactional data. And, of course, to process this data effectively you will also need analytics, which deal with all the intricacies, at your disposal.

FINCAD provides the tools to create high-quality interest rate curves and models, giving you new insights that enable you to be proactive about the Libor transition. Understanding how Libor is trading relative to ISDA fallback protocols is one piece of the picture. But seeing the complete interest rate models enables you to look through these valuations and into the underlying market risk factors. This information can help you understand where these factors may change, perhaps drastically, for your individual firm.

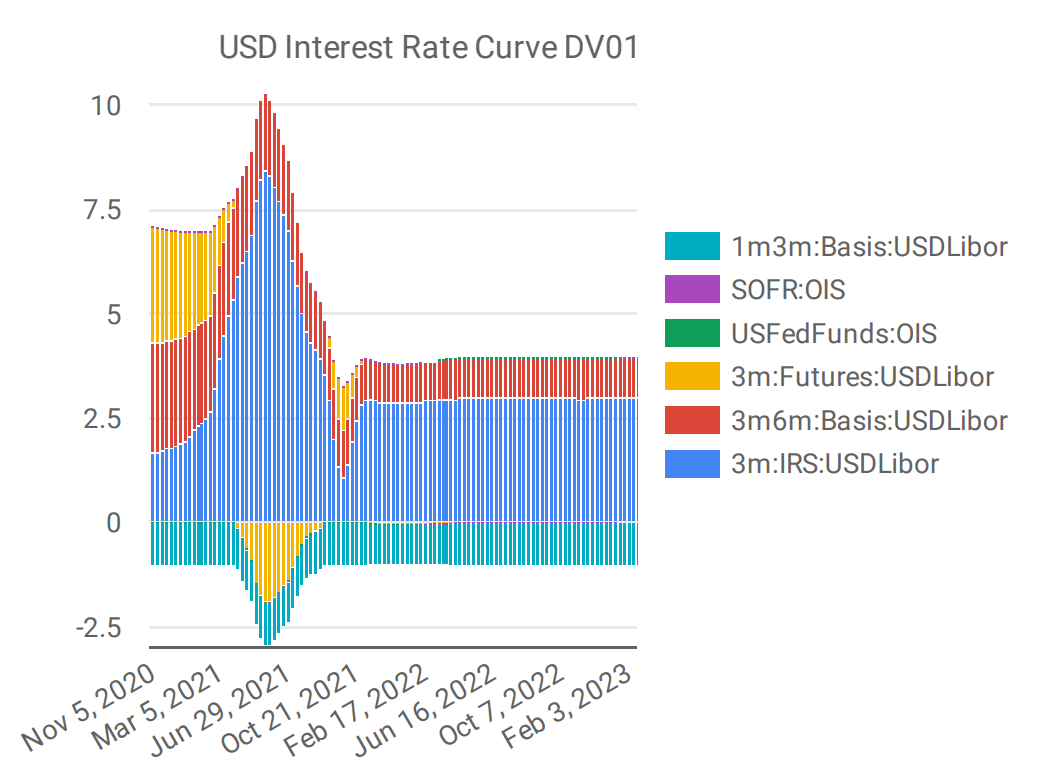

As an example, the graph below depicts a useful metric –the unscaled DVO1, showing forward rates at each time point, aggregated across all sub-curves in USD. This metric shows the breakdown of the instruments and how they drive the shape of the curves.

When we then apply the ISDA protocol fallback to replace Libor with alternative rates and spread adjustments, for each point on the forward curve, we can demonstrate the impact to the underlying drivers of market risk hedges, with respect to the market data instruments and maturities.

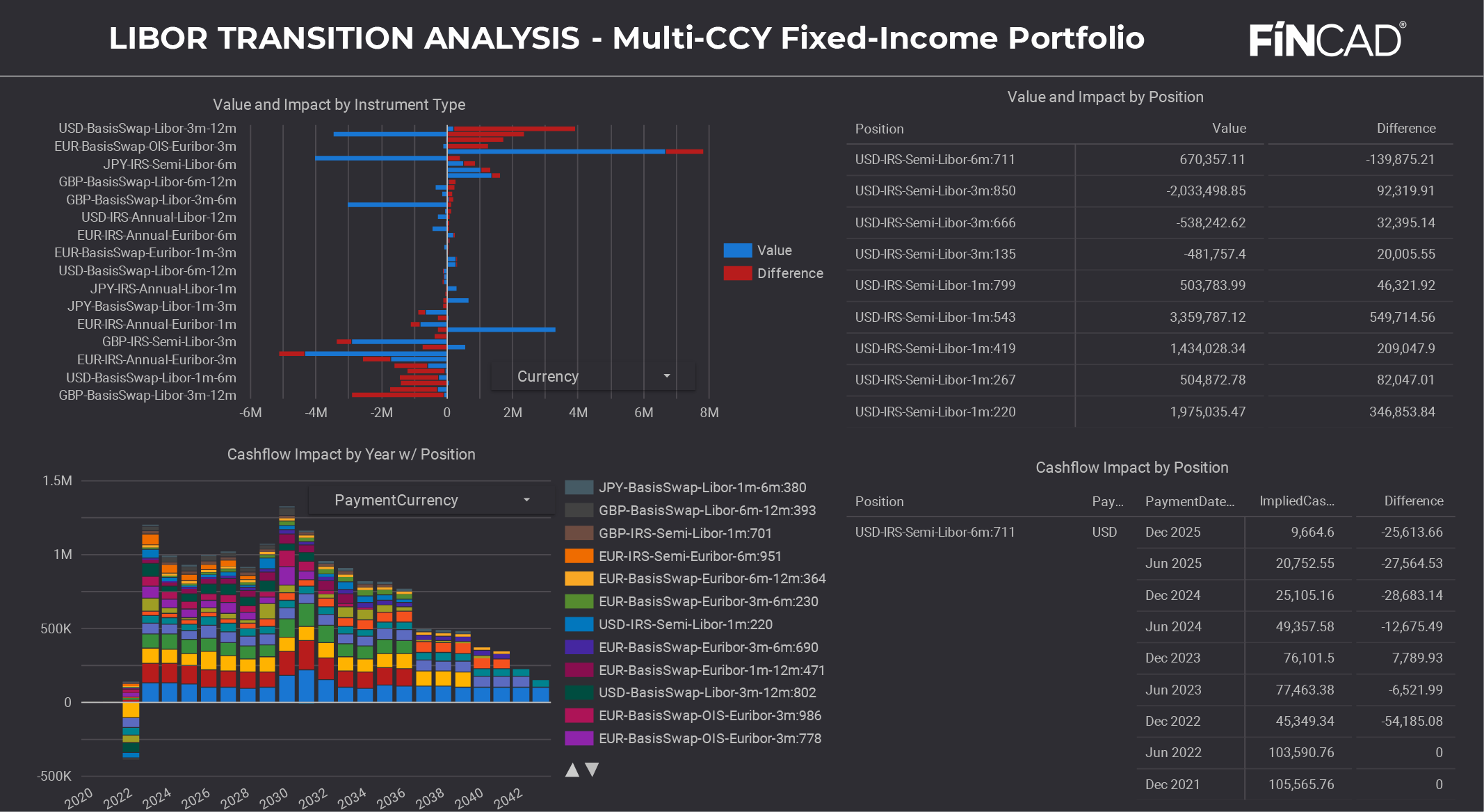

FINCAD can also provide you with detailed portfolio-level analysis, as shown below for a multi-currency, fixed-income portfolio. The value and impact by position are ranked in red in the top graph and the impact to projected cash flows is represented in the bottom graph.

In the end, there could be some surprises lurking, potentially in some of your more complex arrangements. But the true power of leveraging high quality data and robust analytics is not just gaining more insight into the change that awaits you in 2022 and beyond, but also in empowering you to seek better ways to make Libor transition successful for your organization.

Have these takeaways piqued your interest?

Get the full story including detailed analysis of the transition for USD, EUR, JPY rates and view specific multi-currency examples by listening to our on-demand webinar recording. Also, be sure to download your complementary copy of our brand-new white paper, “Inside the Libor Transition: Combining High Quality Market Data and Powerful Financial Analytics.” You’ll get the latest research on how you can harness the power of data and analytics to tackle the Libor transition.

For further information or if you'd like to speak to a FINCAD financial engineer, please click here. Or, click here to request a demo.