Do you have interest rate swaps with exposure to Libor fixings beyond 2021? If so, you may have cause for concern. Valuing these positions requires published Libor fixings, and after 2021 Libor is likely to be discontinued. The reality is that these fixings may never arrive.

When we reach the point where Libor is no longer published, this will immediately trigger fallback clauses in the existing contracts. These fallback clauses must then be properly understood and handled by the systems and technology supporting these legacy Libor positions at that time. But many firms’ technology is not fully equipped to support this changeover.

Instead, what if you could avoid this headache by making the transition away from Libor well ahead of 2021? In fact, many firms and investors are already making the switch to the new risk-free rates, which are more robust funding benchmarks. Even if switching away from Libor positions early may lead to some costs in the short-term, for many, getting this done ahead of the looming 2021 horizon is still a wise choice.

At first glance, there are a few options on how to go about getting rid of Libor from swaps/futures books. An obvious way to convert the long-dated interest rate swaps from Libor is to unwind and restrike. However, this could be extremely costly if the positions are far out of the money. Another way forward, which can avoid this problem, is to take advantage of the growing liquidity in basis swaps, which exchange Libor for alternative rates.

If you can structure new basis swap positions to perfectly align with existing Libor fixings in your portfolio, you can use the basis markets to swap out of Libor positions and into alternative rates. However, to even consider the possibility would involve an extensive task to find all the basis swap trades that would be needed to remove Libor exposure after 2021. It is unclear if there is a one-size-fits-all solution to this business challenge. And even if there was, many firms may still not have the time, resources, or technology needed to carry out a basis-swap exit from Libor.

In this situation, having the right pricing and risk analytics makes all the difference. Using FINCAD F3, you can analyze your books and automatically discover the basis swap positions needed to remove Libor exposures. And because it is based on FINCAD’s Universal Algorithmic Differentiation™, this analysis is lightning-fast and can be performed on any portfolio.

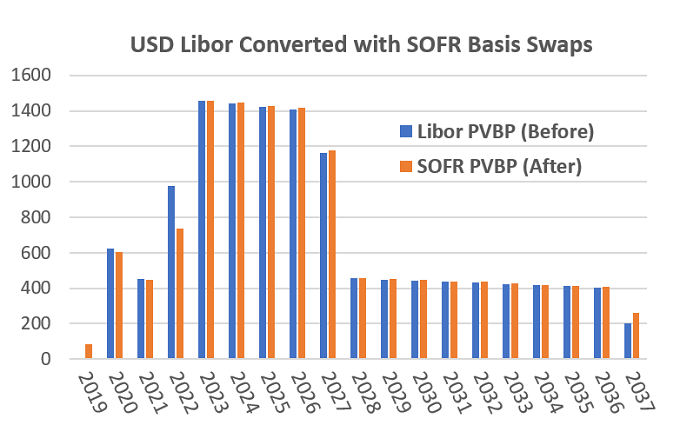

An example is shown in the figure below, which demonstrates the results of adding an aggregate position in newly traded Libor-SOFR basis swaps to an existing $100MM notional book composed of interest rate swaps and ED futures. By combining with the results obtained from FINCAD F3, a completely Libor-free portfolio is obtained, all with a SOFR PVBP profile that is very similar to the original Libor risk profile.

There are clear benefits to getting away from Libor positions early. These include having ample time to adequately test systems and operations around alternative rate positions, and having the opportunity to reduce uncertainty around the impact of Libor’s end. However, it can still be a difficult undertaking. This is yet another reason why having the right technology and tools available is paramount. These will equip you with everything you need to explore all the possible routes for preparing for the end of Libor.

For more information on how FINCAD F3 helps firms prepare for the transition to new risk-free rates, check out our technical document: FINCAD F3 – Ready for the End of Libor