Last weekend, the clearing houses changed their pricing methodology on $80 trillion in Libor interest-rate swaps by switching to a new benchmark rate, known as the secured overnight financing rate, or SOFR, for the purpose of discounting the cashflows. Previously the Fed Funds rate was used for discounting.

The switch, which was referred to in a recent Bloomberg article as a “big bang” is anticipated to increase longer-term liquidity in the new benchmark. But, according to the article, there are also concerns over unpredictable pricing activity, with the SOFR switch projected to spark the sale of tens of billions of dollars of swaps.

Are the Latest Fears Founded?

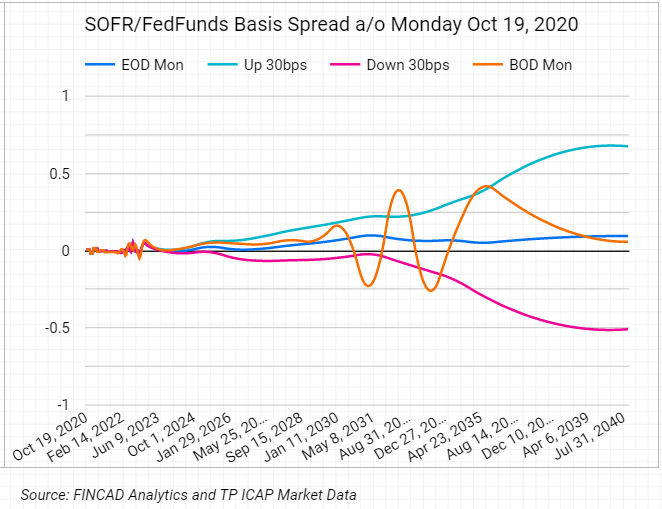

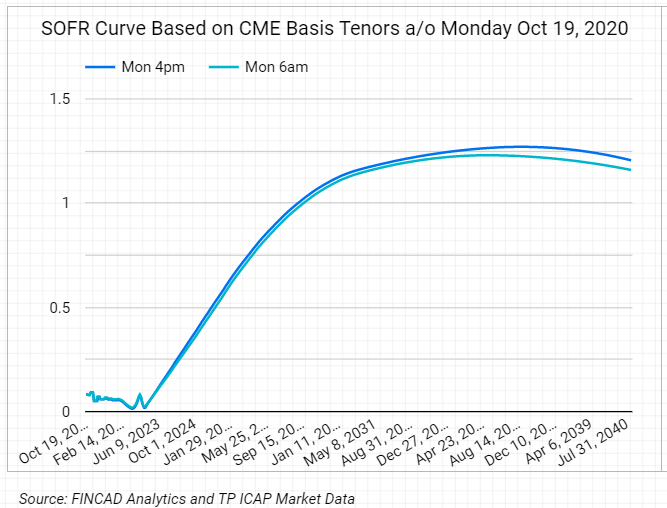

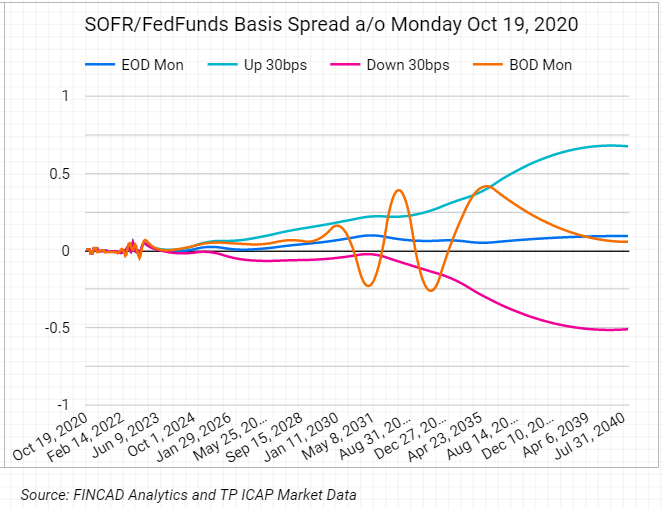

Despite fears that have circulated of effects to the markets from the SOFR discounting transition, it is unlikely to have a major impact. We can simulate the impact of the large number of basis trades hitting the market this week by synthesizing the SOFR/FedFunds basis and applying widening spreads up to 30 basis points on these basis swaps across the 2y through 30y maturities that are being offered by CME. This is represented in the figures below.

Early on Monday these impacts were present in long-dated maturities, but did not affect any near-term market activity. Despite the concerns that have been raised as late as last week, we can see the end of day SOFR curve and spreads from Monday quickly returned to well within the norm. The auctions and market activity around these basis swaps seems to be of limited enough importance to prevent any real catastrophe in this case.

Overcoming Challenges of SOFR Transitioning

While the recent ‘big bang’ move to SOFR discounting is unlikely to rattle the markets to the degree some speculate, firms still need to position themselves to be resilient to market change. When it comes to transitioning away from Libor swaps and other Libor-linked instruments, participants are bound to encounter various challenges. To proceed efficiently and get all the information needed, firms will face a series of curve-building and pricing system changes, together with a need to accommodate many new instruments, often with differing liquidity profiles. Without the right tools to accurately value and risk manage Libor-linked and alternative rate portfolios, they will face risks much greater than just the basis market activity early this week.

At FINCAD, we are heavily involved in helping clients transition to the new alternative risk-free rates (RFR’s), including SOFR. In fact, we have been integral to the entire transition process for many of them, through ensuring that their valuation and risk systems, and curve-building frameworks, are ready and able to cope with the transition.

Indeed, FINCAD users are ARR-ready with no changes to their technology needed. And those clients who use our hosted services get switched to the new ARR’s, including SOFR, automatically, with FINCAD taking care of all related changing data sources and function calls for them. Leaving the transition to FINCAD, enables firms to push forward with business as usual, eliminating disruption to their operation.

How FINCAD Helps

FINCAD offers best-of-breed technologies for pricing, modeling and risk analytics, that are cloud-enabled, future-proof and offer the widest range of instrument capabilities on the market. FINCAD has embraced cloud platforms for many years and used them to develop, market test, and deliver our analytics. Cloud offers many well-known advantages to financial institutions, such as ease of use and scalability, strong security, and a faster time to market for new features and changes—to name just a few. These are all advantages key to a successful Libor transition.

Our people have also been integral in helping clients transition away from Libor. FINCAD solutions are backed by expert financial and software engineers, who have decades of experience, and are fully committed to helping facilitate our clients’ success.

Through FINCAD’s market data integration, we also help firms understand both the future cash flow impact, as well as today’s profit and loss (PnL) impact of switching to SOFR. This approach empowers firms to, for example, devise a hedging strategy that will minimize any shortfall related to the transition. High-quality data and analytics also allow our clients to run all the reports they need to help them create a bullet-proof SOFR transition strategy.

Value of Future-Proofing

As regulations and the overall financial markets evolve and innovate, the need for solutions that provide utmost flexibility for change increases. FINCAD solutions are future-proof and will enable you to meet changes involved with Libor transitioning and any other market changes that inevitably come your way. FINCAD covers every ARR and RFR such as SOFR, SONIA, €STR, TONAR, SARON, including any additional rates that crop up in the future.

Check out our other Libor blog posts for more information:

Gearing Up for the End of IBOR

Connecting the SOFR Curve to SOFR Swaps

Building a SOFR curve was easy!