Some big changes are on the horizon for 2020. CME and LCH have both announced plans to change the USD discount rate by shifting their price alignment interest (PAI) to SOFR in October. Unfortunately, many remain unaware that this transition will have immediate impact on the value of OTC Libor swaps.

So, what will the CME/LCH changes mean for those affected? For any open positions on CME or LCH, the PAI transition will be accompanied by a cash compensation, for any value change that results for end-users. If the value of your position increases, you will still have to post additional margin or face early liquidation of your positions. My recent technical paper shows how to determine the expected compensations at the future transition point, which provides the link between current Fed Funds OIS discounting and a future with SOFR discounting. Generally the compensation amount will be small though, meaning this is likely to be more of a minor inconvenience than anything to worry about.

Since the SOFR discounting impact is to be compensated, this will cover both the direct MTM value impact and the impact to forward curves. The way Libor curves are built assumes a given discount rate, forward rates and/or par swap rates, which will be impacted later this year when the discount rate changes to SOFR. This is one way that OTC swaps will be effected. However, the impact is again likely to be minor because the influence of discounting on forward curve construction is muted and the basis between SOFR and Fed Funds is not very large.

However, there is another important issue for us to consider regarding OTC Libor swaps. Trades under CSAs that remain on Fed Funds discounting will be impacted as a result of the volatile basis between SOFR and Fed Funds. In my paper, I show that indeed any Libor trades that do not switch to SOFR discounting at the same time as CME and LCH next year can be impacted today by a convexity adjustment. This is based on a few assumptions:

- MTM impacts are fully compensated for exchange-cleared swap positions

- Forward curves are calibrated from liquid exchange-cleared swap rates

- Centrally cleared, SOFR discounted swaps will be used for hedging OTC positions

- Assuming Vasicek model and 1% volatility for term structure of SOFR and Fed Funds

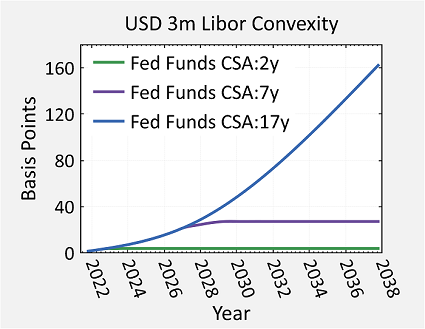

I used the results in my paper to do an analysis on the impact for 3-month Libor for OTC swaps that continue to use Fed Funds discounting. These results are shown in the figure at right. There are three curves which represent three different time horizons for transitioning OTC swap CSAs to SOFR discounting, including 2y, 7y and 17y after CME makes its transition to SOFR PAI.

For short maturities the impact starts off small, but becomes much larger for cashflows out to 20 years and beyond—with a very sizeable impact for the long maturities. This effect is due to the basis risk between Fed Funds and SOFR that must be included in the OTC positions in this scenario. It is important to realize that without considering this basis risk, you may already be mispricing your long-term OTC Libor swaps that are not shifting CSAs to SOFR discounting, along with the CME and LCH PAI transition.

What will happen in the EU? In the European Union, perhaps regulators will transition EONIA to €STR in a way where everything switches simultaneously and MTM impacts are also compensated. This would avoid impact to OTC swaps. However, given that SOFR and Fed Funds will coexist for some time, it may be a much larger issue for USD OTC Libor swaps that remain on Fed Funds discounting. The results above show that the longer you wait to transition CSAs to SOFR discounting, the bigger the impact will be. Right now it seems prudent for investors in both regions to take steps to align OTC CSAs with the transition to SOFR and €STR discounting in order to prevent unwanted MTM impacts.

Lastly, I’d like to point out that FINCAD F3 can help manage the transition to alternative rates, such as SOFR and others. In fact, I’ve recently been working with our developers on building out features so that our clients can easily perform analysis of OTC positions (similar to the above) using FINCAD F3. I hope those of you who are clients find these features useful.

In the meantime, happy 2020! Best wishes to all of our readers for a year full of successful trading ahead!

For more on Libor, check out these blogs:

Building a SOFR curve was easy!

Eliminating the SOFR Basis: What Do We Lose?

Using the Basis Swap Markets to Prepare for Libor’s End